Despite the claims of being at the end of the Great Recession, macroeconomics has still to achieve the changes, promised during the crisis. Not only has it not progressed in terms of theory and modelling, the impression is (as stated by, for example, Tony Lawson) it is in a "sort of mess". Big mess. Among the ideas that sprang as more important than before the crisis are surely also the ideas of Hyman Minsky. Below, we review a recent working paper of Nikolaidi and Stockhammer, who overview existing applications in economics, using Minskian ideas.

Hyman P. Minsky was an American economist whose research attempted to provide an understanding and explanation of the characteristics of financial crises, which he attributed to swings in a potentially fragile financial system. Although he considered himself a Keynesian, Minsky was uncomfortable with the way most mainstream economists interpreted Keynes. He rejected conventional economic ideas such as the efficient market hypothesis in favor of what he called the financial instability hypothesis. Minsky held that, over a prolonged period of prosperity, investors take on more and more risk, until lending exceeds what borrowers can pay off from their incoming revenues. When overindebted investors are forced to sell even their less-speculative positions to make good on their loans, markets spiral lower and create a severe demand for cash—an event that has come to be known as a "Minsky moment." In general, his economic theories were largely ignored for decades, until the financial crisis of 2008 caused a renewed interest in them.

Minsky is largely known for an advocate of the financial instability hypothesis (FIH), with both empirical and theoretical aspects. The readily observed empirical aspect is that, from time to time, capitalist economies exhibit inflations and debt deflations which seem to have the potential to spin out of control. In such processes the economic system's reactions to a movement of the economy amplify the movement--inflation feeds upon inflation and debt-deflation feeds upon debt-deflation. Government interventions aimed to contain the deterioration seem to have been inept in some of the historical crises. These historical episodes are evidence supporting the view that the economy does not always conform to the classic precepts of Smith and Walras: they implied that the economy can best be understood by assuming that it is constantly an equilibrium seeking and sustaining system.

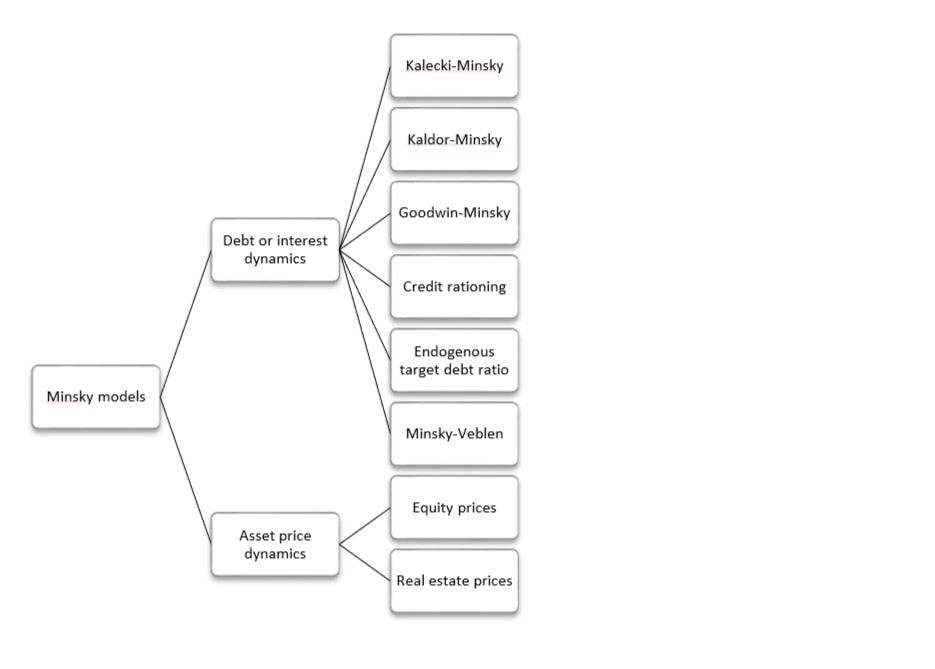

In a recent working paper (click) of the Post-Keynesian Economic Study Group (PKSG), Maria Nikolaidi and Engelbert Stockhammer provide a systematic overview of the literature on the usage of Minskian models in economics. They separate the models into several broad categories: models that focus on the dynamics of debt or interest, with no or a secondary role for asset prices, and the models in which asset prices play a key role in the dynamic behaviour of the economy. Within the first category of models they make a classification between (i) the Kalecki-Minsky models, (ii) the Kaldor-Minsky models, (iii) the Goodwin-Minsky models, (iv) the credit rationing Minsky models, (v) the endogenous target debt ratio models and (vi) the Minsky-Veblen models. Within the second category of models, they distinguish between (i) the equity price Minsky models and (ii) the real estate price Minsky models.

The Kalecki-Minsky models constitute the first group of debt or interest dynamics models. In them, the output is demand determined, the standard Keynesian stability condition on the goods market holds - marginal propensity to save is larger than the marginal propensity to invest - while asset prices and household debt are assumed away. In these models the debt-to-capital ratio is used as an indicator of financial fragility. Many of these models (e.g. Lima and Meirelles, 2007; Nishi, 2012; Sasaki and Fujita, 2012) measure the financial fragility of firms by using Minsky’s classification of hedge, speculative and Ponzi finance regimes based on the relationship between investment expenditures, profits and interest payments. In the majority of the Kalecki-Minsky models the interest rate is endogenous. The interest rates are set by commercial banks which increase in response to the rising debt-to-capital ratios of their costumers (e.g. Charles, 2008) or because of increasing economic activity (e.g. Lima and Meirelles, 2007). With the exception of Fazzari and colleagues (2008), in such models, the labour market is not explicitly analysed.

The second group within the debt or interest dynamics models are the Kaldor-Minsky models. Kaldor (1940) proposed a model where the goods market is overshooting because of strong accelerator effects (opposite to Kalecki-Minsky models, the marginal propensity to invest is greater than MPS). While in Kaldor and other related literature investment levels out at some point because of real constraints (e.g. supply side bottle necks), the Kaldor-Minsky model “is made unstable by a strong investment accelerator, but the instability is contained by financial forces” (Foley, 1987: 364). In most Kaldor-Minsky models the interest rate is endogenous (e.g. Foley, 1987). However, there are also models in which the interest rate is exogenous (e.g. Skott, 1994).

The third group is the Goodwin-Minsky models. Goodwin (1967) examined the cycles that can be generated by the interaction of wage share and employment rate. In his framework the Say’s law holds and output is determined by capital stock. In the Goodwin-Minsky models debt is introduced via an investment function and interest payments squeeze profits and investment in the same way that wages do in the Goodwin model. A key difference of the Goodwin-Minsky models from the Kalecki-Minsky and the Kaldor-Minsky models is that labour market plays a central role via the Marxian idea of the reserve army of labour.

The fourth group is the credit rationing Minsky models. In contrast to the previous models, banks in these models apply credit rationing explicitly and this credit rationing is affected by banks’ financial position. Credit rationing refers either to the volume of credit that is supplied by banks (Ryoo, 2013b; Nikolaidi, 2014) or to the interest rate that is charged by banks which in turn affects the amount of credit (Delli Gatti et al., 2005, 2010). In these models the interaction between the financial position of firms and the financial position of banks plays a central role in the emergence of cycles and instability.

The fifth group is the endogenous target debt ratio models (Dafermos, 2017; Jump et al., 2017). In these models the expenditures of the private sector and the dynamics of debt are affected by stockflow norms (target debt ratios). These stock-flow norms change endogenously based on the Minskyan argument that the perception of risk alters during the economic cycle: in a period of tranquil or high growth firms, or the private sector in general, increase their target of debt; the opposite is true during period of low or volatile growth. This endogeneity of the target debt ratios is conducive to cycles and instability.

Finally, the sixth group is the Minsky-Veblen models. Applying Veblen’s (1970 [1899]) ideas about the impact of social conventions on consumption, the Minsky-Veblen models assume that low-income households take on consumer debt in order to increase their consumption expenditures and emulate the high-income households (Kapeller and Schütz, 2014; Ryoo and Kim, 2014; Kapeller et al., 2016).

Within the group of asset price dynamics models ,the first type is the equity price Minsky models. In these models households invest in different financial assets, including equities, and their portfolio choice affects the equity price dynamics. The expected rate of return on equity plays a key role in generating instability or endogenous cycles (see e.g. Taylor and O’Connell, 1985; Ryoo 2010, 2013a; Chiarella and Di Guilmi, 2011). When the expected rate of return increases, the price of equities goes up and this affects positively economic activity via investment and/or consumption.

The second type of asset price models (a more rare one) are the real estate price Minsky models. These models have been motivated by the global financial crisis and focus on the role of housing prices in the emergence of instability and cycles (Ryoo, 2016). House prices affect the provision of mortgages (since houses are used as collateral in the debt contracts). As mortgages increase, the demand for houses increases leading to further increases in the price of houses. As in the Minsky-Veblen models, the boom stops because of the rise in household indebtedness.

In total, there is an impression Minskian models are still to achieve stronger development, rigor and empirical applications in heterodox and mainstream economics (the paper lists also some applications, combining Minskian assumptions with mainstream modelling, based on DSGE approaches). With the advent of the crisis, it has become clear macroeconomic modelling needs renewal both in terms of theoretical assumptions, mathematical modellings and empirical profoundness. Minsky's theories can offer all of those and it is hoped for they will achieve a larger "audience" and more frequent, broad and consistent theoretical and empirical work.

Written by: Andrej Srakar.

RSS Feed

RSS Feed